{kind=link}

CCP recently released the Monthly Economic Report for July 2017. It is interesting. Here, we don’t try to divine fleet movements or the like. We just look at what the report appears to show us economically.

{kind=link}

Initial Assessment

Much of an assessment has to be taken with a grain of salt. The EVE MER makes no assumptions or has any referencing for seasonal adjustment. There are no quarterly or monthly comparisons made for the player as presented by CCP. Perhaps that is something we here at INN will get into more as we expand our coverage of the MER in the future.

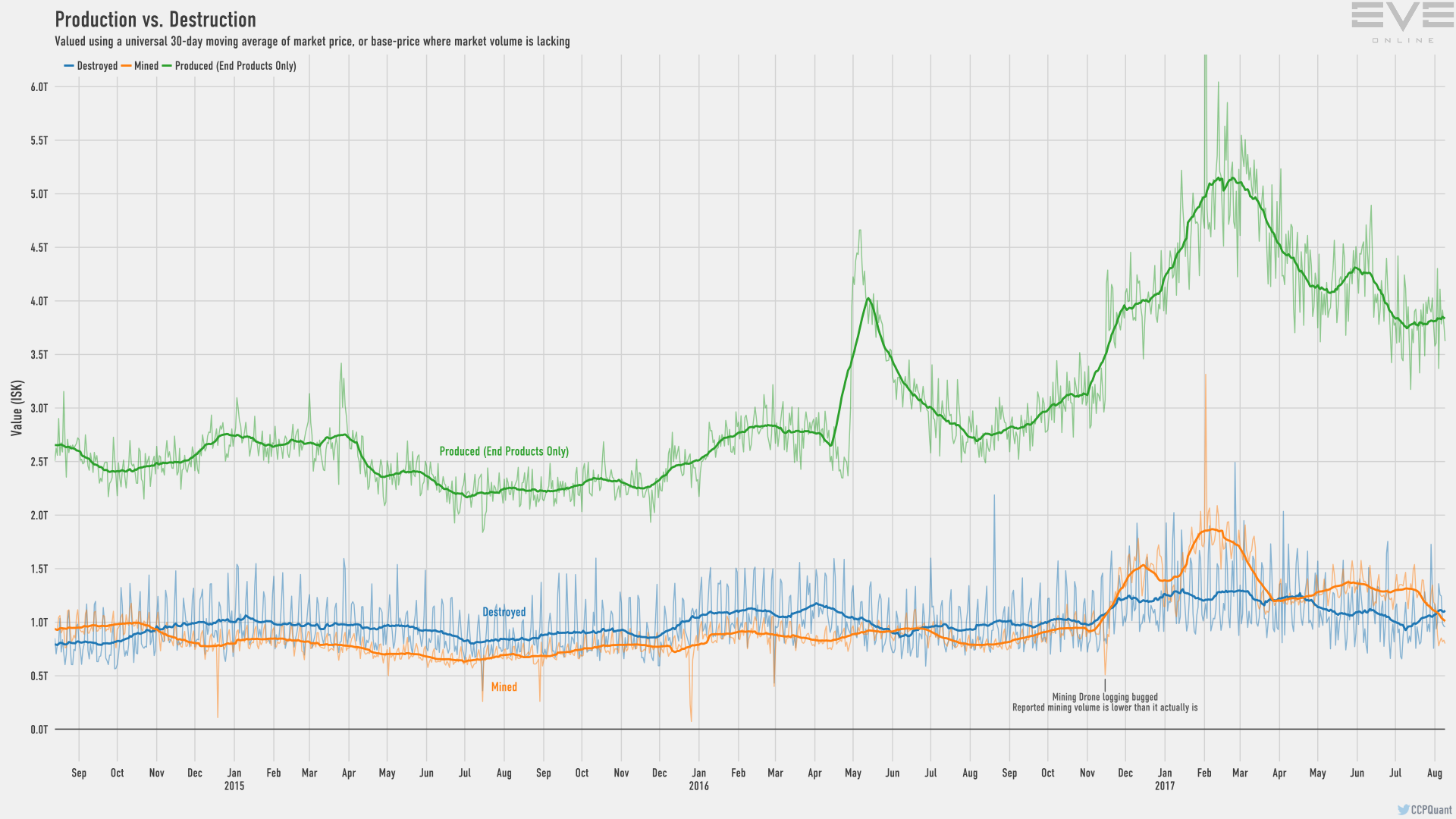

Production leveled off after its steep decline since March with a brief bump in May. For a game in decline, EVE Online shows remarkable resilience in the production area.

Mining fell off a cliff in the last third of July. If this is a result of The Imperium prepping for war, a seasonal impact of summer or a combination of both is yet to be seen as we get the August numbers next month.

Amount Destroyed picked back up after a steady but gradual decline since mid-April. It had moved near a more nominal range but seems to be edging closer to the higher levels we have seen since mid-November 2016.

Delve

Key Economic Figures (Click to Enlarge)

The biggest stand out to many will be the whopping 21% increase in mining output in Delve.

NPC bounties were up 4% with Net Imports dropping -10%. The import activity is to be expected during a gear up to war.

Equally impressive to the mining numbers where Production and Trade. These were up 36% and 14% respectively.

But those are the bellwether indicators that lead to an autonomous Nullsec. We are not there yet. But Delve is closer to that realization that CCP had just prior to the release of FozzieSOV.

When you look at Delve, you now see the third largest market in EVE. It is now the largest production center, the second largest importer, and an all around hub of activity. If Jita is the Kaitain of Eve, Delve is quickly becoming its Arrakis. Goonswarm Federation alone has grown by an average of 5.5% a month since January 2017. Needless to say, The Imperium is growing.

MER Numbers in General

This brings me to a point I have made before in reference to the numbers in the MER. Comparing region to region is a pointless endeavor. Unless you are normalizing for population, the raw data in the MER may not be the best source to base game mechanic decisions on.

Bounty Prizes is way down since the change to fighters. While Delve showed an increase, the predicted effect across EVE to smaller groups was notable. With Incursion payouts, manufacturing, Transaction tax, and Brokers fees all down in July, we have to believe there is something going on. This month most of those factors all dropped more significantly than the same time period in previous years. Time will tell if these bounce back.

Player Base

Many things can affect the market in EVE. For one, it is easy to manipulate with little ISK. You cannot underestimate the impact of players preparing for the planned massive change to moon mining and how that impacts players’ decisions within the market.

We are also not privy to subscriber numbers but the 2Q17 PDU according to eve-offline.net has dropped approx -19%. The Imperium striking back in the North hasn’t had a significant impact on that number in the last few weeks. September numbers should give us a more clear picture related to gameplay.

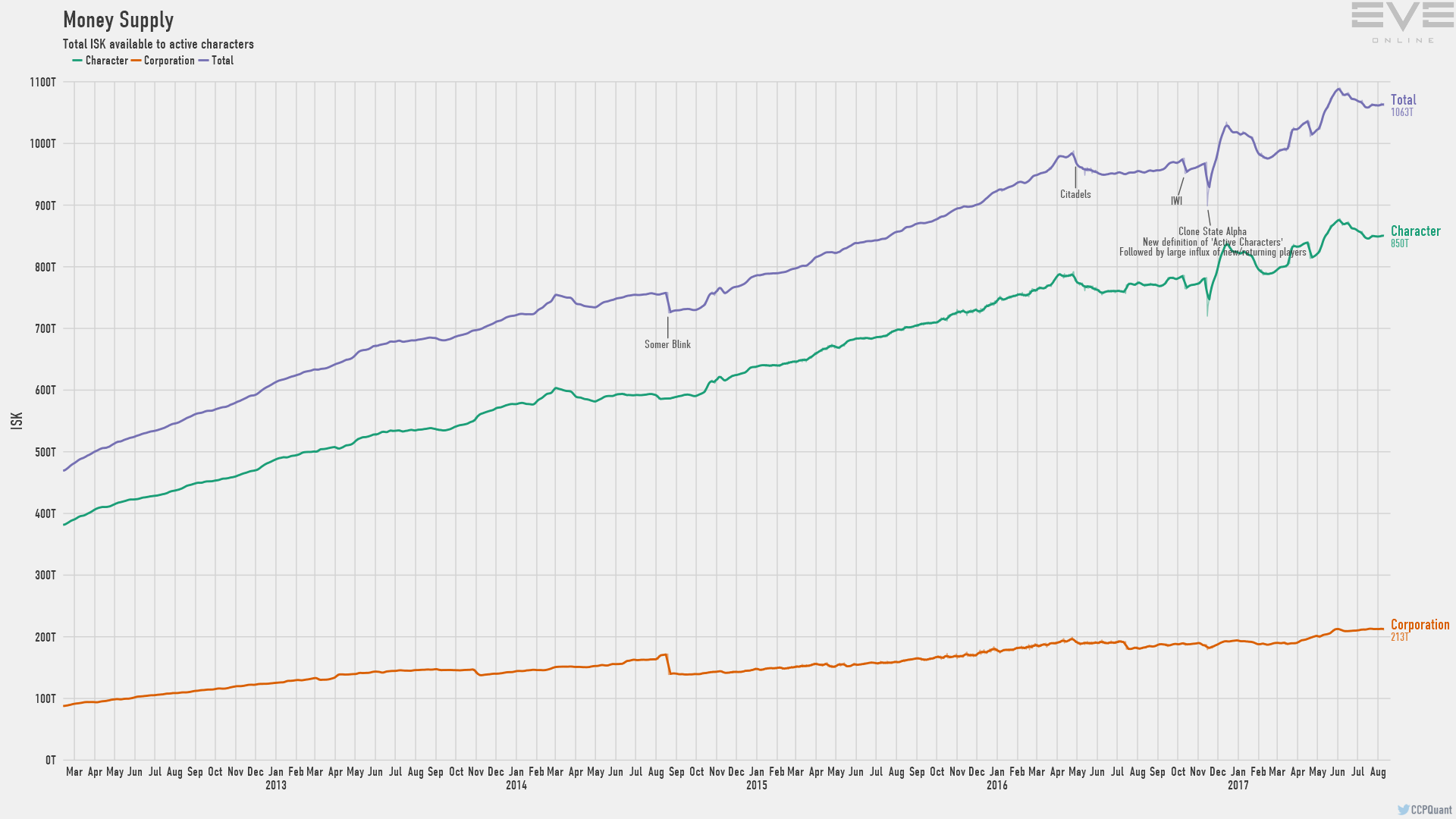

Money Supply

Money Supply (Click to Enlarge)

Looking at the money supply over a short period is never good. Long term trends in this area are what you need to see. Over the last few months, this has leveled out after a short sprint during the first part of 2017.

It is interesting that total and character closely mirror each other, but ISK in corporations seems to show steady growth. Is it behavioral that mega corporations or others are not keeping vast wealth within the corporations and transferring it to characters?

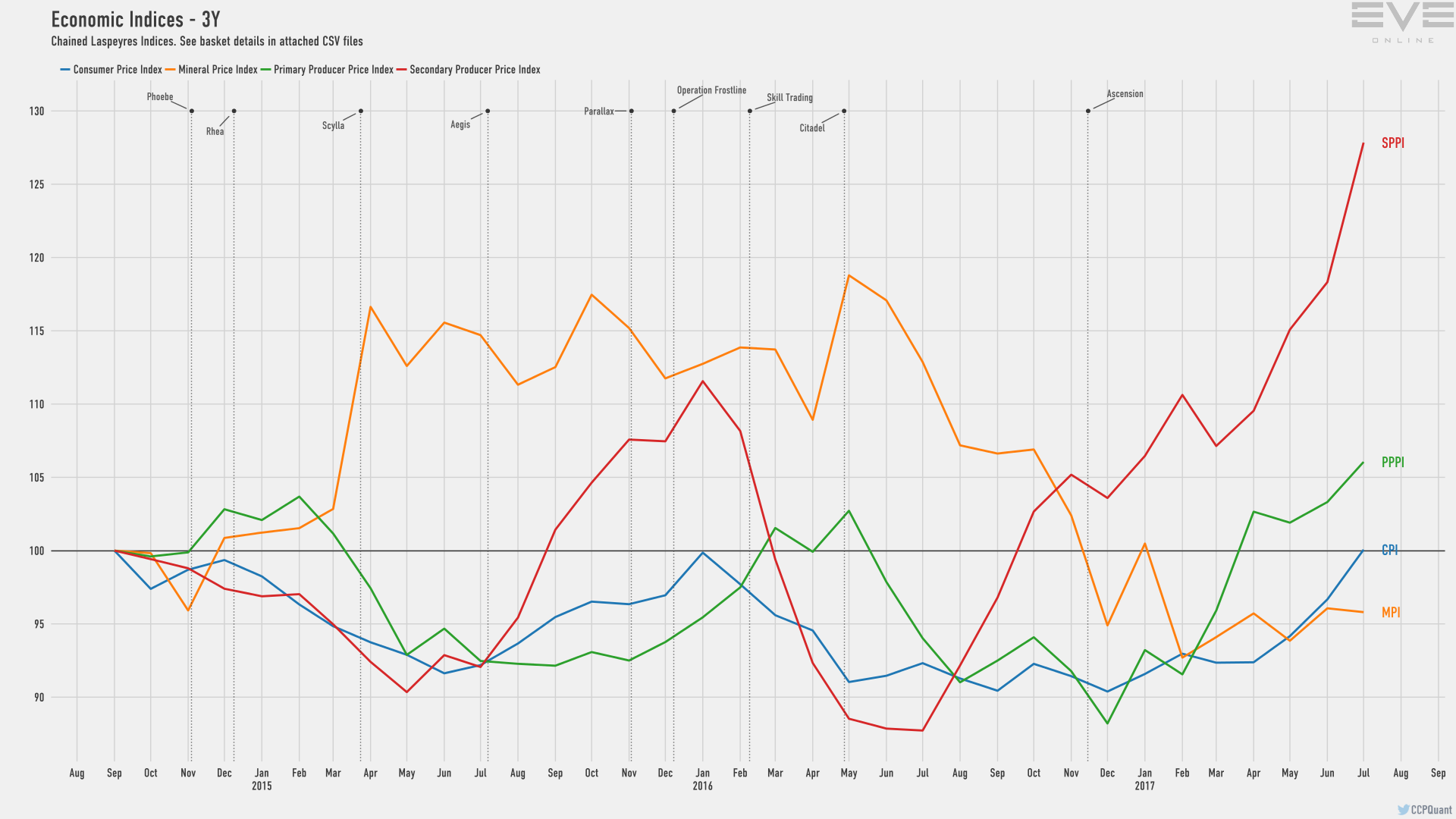

The Indices

Economic Indices (Click to Enlarge)

Looks like the SPPI is continuing its meteoric rise while the CPI and PPPI experience significant increases.

The MPI or mineral index seems to have leveled off from its decline this year.

Summary

As 3Q17 gets under way in EVE, Delve is overshadowing all other gains and hiding them. Unless you are looking under the covers at estimated per capita numbers, it is hard to know what activity mechanics are really impacting the economy. Sure, you can make some generalizations.

While changes have been made, it seems the industrial might of the numbers game is in Delve’s favor.

If you build it, they will come.